The biggest property tax reform in 25 years. Here is what it actually does to your portfolio.

Three changes. Three start dates. Three investor profiles that respond very differently. A CFA-qualified buyer's agent and a chartered tax accountant walked 280 investors through this on Thursday night. The full briefing and the recording are below.

Published: 15 May 2026

Read time: 12 minutes

Recording: 120 minutes

Co-presented: Get RARE Properties & AceBiz Accounting

Co-presenters of the briefing: Manpreet Singh, CA (left), and Rasti Vaibhav, CFA (right).

Status: announced, not yet law

Every measure on this page is subject to consultation and parliamentary passage. We are deliberately not telling anyone to sell, restructure or buy in response to a press release. The job right now is to understand where you sit, document what needs documenting, and wait for the draft legislation before doing anything irreversible.

The big picture

Three changes in sixty seconds

Treasury announced three measures on 12 May 2026. They start on three different dates, hit three different groups, and most of the news coverage so far has flattened them into a single story. They are not a single story.

01

Negative gearing

Restricted to new builds

Losses on existing rentals bought after Budget night can only offset other property income. Excess losses carry forward. They no longer reduce wages or business income.

Starts 1 July 2027

02

Capital gains tax

50% discount replaced

Replaced by inflation indexation plus a 30% minimum tax on real gains. Applies to all assets except new builds, which can choose either method.

Starts 1 July 2027

03

Discretionary trusts

30% minimum tax

Trustees pay 30% on trust income before it reaches a beneficiary. Non-corporate beneficiaries get a credit. Bucket companies get none. SMSFs and fixed trusts are excluded.

Starts 1 July 2028

Source: Treasury Fact Sheets, 12 May 2026. Anything framing this as a single "investor crackdown" has missed the point. Each measure behaves differently, starts at a different time, and applies to a different cohort.

Find yourself

Which one are you?

The reform behaves very differently depending on where you sit. Three composite profiles cover most situations. Pick the closest match and read that section first.

These are composites, not real clients. Your actual situation will sit somewhere along this spectrum and may overlap two profiles.

Profile 01 · Existing investor

Sarah is worried about nothing.

Sarah is a marketing manager on $180k, owns one rental bought in 2023, currently negatively geared by around $11,500 a year. No plans to sell. The headlines have her panicking. They shouldn't.

"My property is negatively geared. Do I lose that deduction in 2027?"

No. Properties owned before 12 May 2026 are grandfathered for the life of the asset. Sarah keeps negative gearing exactly as it works today. Her roughly $5,400 a year in tax savings continues. The change applies only to properties purchased after Budget night.

The CGT change is more subtle but still benign. When Sarah eventually sells, her gain gets split in two. The portion accrued up to 30 June 2027 keeps the old 50% discount. The portion accrued from 1 July 2027 onwards uses the new indexation method. It is not retrospective. The gain she earned under today's rules keeps today's treatment.

Annual tax impact while she holds

$0

No change to ongoing deductions

Negative gearing retained

$5,400

Per year, same as today

Confidence level

High

Grandfathering is explicit

What Sarah should actually do

Get a market valuation documented as close to 1 July 2027 as practical. This is the line between the two CGT methods.

Keep records of capital improvements made post-2027 separately. They become more important under indexation.

Do not sell to "lock in" the 50% discount on her existing gain. Holding is almost always better than realising tax now.

If she wants to add a second property, the buy-new-or-established decision is now genuinely different. See James, below.

Profile 02 · Prospective investor

James faces an actual decision.

James is an IT consultant on $220k, buying his first investment property at around $750k. The reform genuinely changes his maths. He has two paths and the right answer depends on more than tax alone.

"Should I buy an established property or a new build?"

If James buys an established property after Budget night, his $14k rental loss gets ring-fenced from 1 July 2027 onwards. It can only offset other property income, not his wages. That removes around $6,580 a year in tax savings until the property is cash-flow positive or sold.

If he buys a new build, negative gearing continues to apply against all income, and he gets to choose between the 50% discount and the new indexation method at sale. On tax alone, the new build wins.

Option A · Established

Loss gets ring-fenced

$14k loss · can't offset wages from July 2027

−$6,580

Annual tax saving forgone

Option B · New build

Negative gearing continues

Full deduction · CGT method choice at sale

+$6,580

Equivalent annual tax advantage

Here is where most commentary will stop. We don't. The tax-favoured option is not automatically the wealth-favoured option.

Property Investment Professionals of Australia (PIPA) data on long-run capital growth in Australia is unambiguous: quality established stock has outperformed new builds by 200 to 400 basis points per year in capital growth. Over a 10 to 15 year hold, that compounding gap typically outweighs the early-years tax advantage of the new build. Especially when the new build is a marketed house-and-land package on the city fringe with a rental guarantee and an aggressive depreciation pitch.

What James should actually do

Model both scenarios with real numbers, including a realistic capital growth assumption and 10+ year hold period. Tax is one input. Capital growth is the bigger one.

If new build, only consider supply-constrained urban infill locations with genuine demand and resale liquidity. Skip the fringe house-and-land packages.

If established, factor the ring-fenced losses into cash flow planning. The deduction isn't gone, it's deferred until the property generates income or is sold.

Wait for draft legislation before signing anything time-sensitive. The grandfathering rules for new builds in particular are still being finalised.

Profile 03 · Family group

The Patels need a plan.

The Patels operate through a family trust with two rental properties and a share portfolio. They currently distribute around $145k a year to a non-working spouse and a bucket company. Under the new rules, the same income and same distribution structure costs them materially more.

"Does our family structure still work, and is the bucket company still useful?"

From 1 July 2028, the trustee pays 30% on trust income before any distribution. Non-corporate beneficiaries get a non-refundable credit, capped at their own tax liability. Bucket companies get no credit at all. For the Patels' setup, the change is material.

Total family tax today

$29,300

Current structure

From 1 July 2028

$43,500

Same income, same distribution

Annual difference

+$14,200

Material uplift, year on year

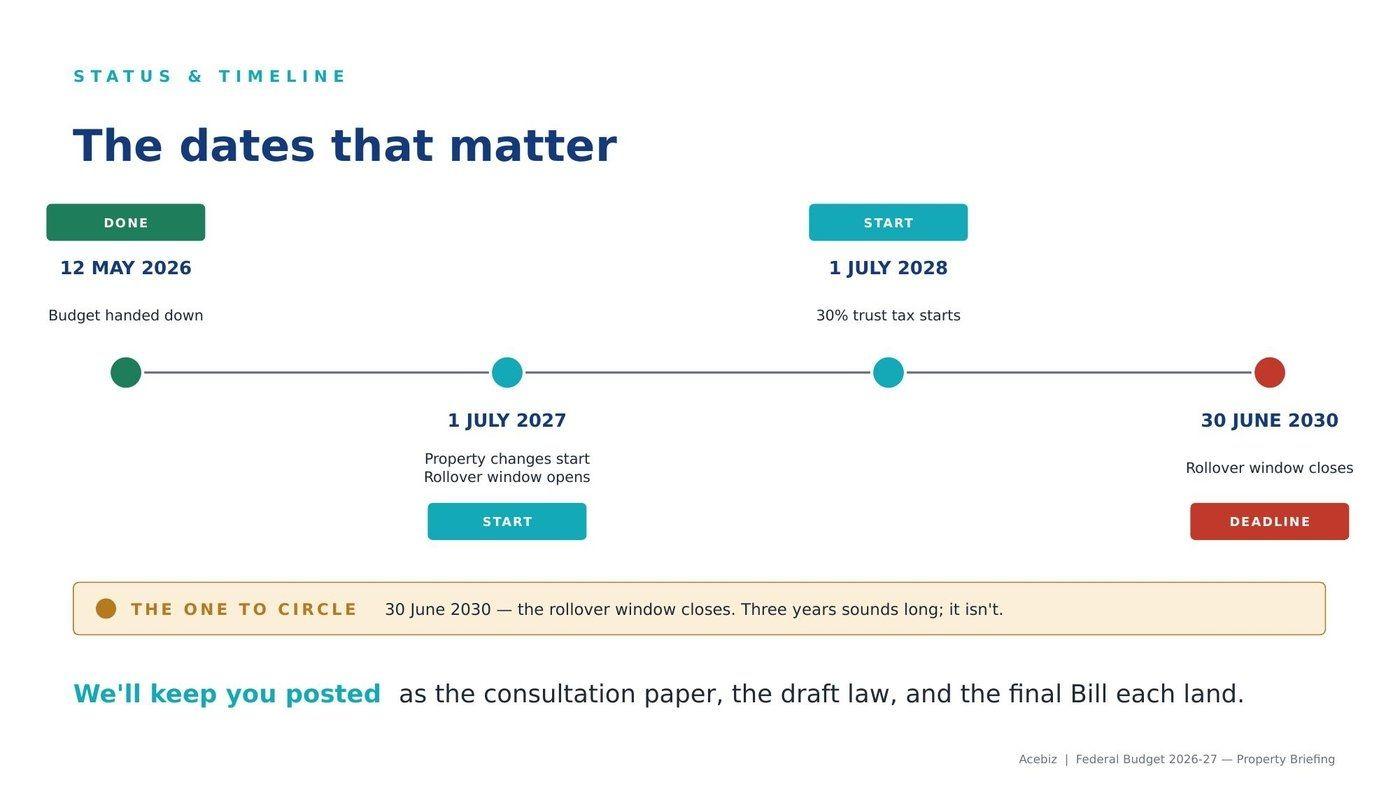

There is a relief valve. Treasury has announced a three-year rollover window from 1 July 2027 to 30 June 2030 to restructure out of a discretionary trust into another entity (typically a company or a fixed trust) without triggering CGT. Three years sounds generous. It isn't, once you account for consultation, draft legislation, advisor capacity, and your own decision-making time.

What the Patels should actually do

Get a current valuation of every trust-held asset on file. This becomes the cost base for any rollover.

Map the family's actual income needs against the trust's distribution flexibility. Sometimes the simplest answer is to distribute more to working family members and less to the bucket company.

Model the three live options: keep the trust and accept the higher tax, distribute differently, or use the rollover to restructure entirely. Each has different long-term costs.

Engage their accountant this calendar year, not in 2027. The rollover window opens 1 July 2027 and good advice is going to be capacity-constrained.

Status & timeline

The dates that matter.

Three measures, three start dates, one rollover window. The date to circle is 30 June 2030 — the trust restructuring window closes.

Two contrarian findings

What the headlines missed.

Indexation can actually be more generous than the old 50% discount.

Most coverage frames the CGT change as straightforwardly bad for investors. For long-hold investors at current inflation rates, that is wrong. Indexation inflates the cost base every year. The longer you hold, the more of your nominal gain becomes "inflation" rather than "real gain", and the less is taxable.

In our 20-year metro-new scenario (full assumptions in the recording), the new indexation method saves about $15,000 in CGT compared to the old 50% discount. The "discount" was never inflation-adjusted. Indexation is. For genuinely long-hold investors, the new method can be the friendlier one.

Existing investors are not fully spared. The CGT change still applies to you.

Most coverage says existing landlords were "spared" from the reform. Half true. Negative gearing was grandfathered for existing investors. The CGT change is not. The post-1 July 2027 portion of any future gain on your existing property uses the new rules. This is why getting a valuation on file at the transition date is the single most universally useful action item on this page, regardless of which profile you fit.

The substance

The hidden rate rise on investor cash flow.

CBA's senior economist Trent Saunders has done the modelling on what removing negative gearing actually does to investor cash flow. The number is large enough to deserve a sentence of its own.

CBA Updated Housing Outlook · May 2026

90–155 bp

"Removing negative gearing is equivalent to roughly a 90 to 155 basis point increase in investor mortgage rates in immediate cash flow terms."

— Trent Saunders, Senior Economist, Commonwealth Bank of Australia

For context: that is larger than the entire RBA tightening cycle that pushed prices sideways in 2022-23. The CBA modelling also suggests listings will fall, because grandfathered owners now have a strong disincentive to sell (selling forfeits their grandfathered treatment forever). Lower listings, in a structurally undersupplied market, generally do not lead to lower prices.

Where to buy now

Regional yields look structurally stronger under the new rules.

The reform hits hardest where yields are lowest. CBA explicitly identifies the most affected investors as those with "high marginal tax rates, high leverage, low rental yields and high interest expenses". That profile is the typical metro buyer. Regional buyers with stronger yields are structurally more resilient.

Metro · Sydney, Melbourne

2.5 – 3.5% gross yield

Higher leverage required. Cash-flow shock larger when negative gearing is removed. Historical capital growth strong but pace decelerating.

Regional · QLD, TAS, WA

5 – 7% gross yield

Lower absolute leverage. Cash-flow neutral or positive. Population shift from capitals continues to support demand.

Get this part right and the tax change matters far less to your portfolio. Get it wrong, and the new rules amplify mistakes you would have made anyway. The job of an investor for the next two years is not to chase tax structure. It is to pick assets that work on the fundamentals, then optimise the tax around them.

The new arithmetic

After 20 years, after tax: not all property is the same property.

Same investor. Same deposit. Twenty years. Negative gearing, depreciation, and CGT all included. The two scenarios below assume the new rules apply throughout.

Metro new build · $700k

3.0% yield · 4.0% growth p.a.

Negative gearing preserved · Full depreciation

$408k

After-tax wealth, 50% discount method

$589k

After-tax wealth, indexation method

Regional established · $700k

5.0% yield · 6.0% growth p.a.

Negative gearing not available · Div 43 only

$1,034k

After-tax wealth, indexation method

Two insights from this. First, asset selection beats tax structure. The regional established option wins by a wide margin even without negative gearing. Second, for the metro new option, the new indexation method actually saves around $15k over the old 50% discount across the full hold period. The reform is not uniformly bad.

Full assumptions and the underlying spreadsheet are in the recording. Source: Get RARE scenario model, May 2026.

Frequently asked

The nine questions investors ask first.

Direct answers to the most common questions. Tap to expand.

What did the Australian Federal Budget 2026 announce about negative gearing?

From 1 July 2027, negative gearing on residential investment property will be restricted to new builds. Losses on established rental properties bought after 12 May 2026 can only offset other property income, not wages.

Properties owned before 12 May 2026 are grandfathered for the life of the asset. Existing investors retain negative gearing on those properties exactly as it works today. Source: Treasury Fact Sheet, 12 May 2026.

Does the CGT change apply to property I already own?

Yes, but only to the gain accrued after 1 July 2027. The 50% CGT discount applies to the gain you built up to 30 June 2027. From 1 July 2027 onwards, your gain uses the new method (indexation plus a 30% minimum tax on the real gain). It is not retrospective.

Existing investors should get a market valuation documented at or near 1 July 2027, as this becomes the line between the two methods.

What is the new 30% minimum tax on discretionary trusts?

From 1 July 2028, trustees of discretionary trusts will pay a minimum 30% tax on the trust's taxable income before any distribution to beneficiaries. Non-corporate beneficiaries receive a non-refundable credit for the tax paid, capped at their own tax liability. Bucket companies receive no credit.

SMSFs, fixed trusts, widely-held trusts, charitable trusts, deceased estates and complying superannuation funds are excluded from the change. A three-year rollover window from 1 July 2027 to 30 June 2030 lets trusts restructure into another entity type without triggering CGT.

Is negative gearing still allowed on new build properties?

Yes. New builds remain fully negatively geared both before and after 1 July 2027. Rental losses on a new build can still be deducted against all other income, including wages.

New build investors also retain the choice between the 50% CGT discount and the new indexation method when selling. A "new build" is defined as a residential property that genuinely adds to housing stock.

Are SMSFs affected by the Federal Budget 2026 property changes?

No. SMSFs and complying superannuation funds are explicitly excluded from all three measures. Negative gearing remains intact inside an SMSF, the 50% CGT discount continues to apply (effective 10% rate in accumulation phase), and the new 30% minimum tax on discretionary trusts does not apply to SMSFs.

What did CBA say about the cash-flow impact of removing negative gearing?

CBA's senior economist Trent Saunders quantified the cash-flow impact at 90 to 155 basis points equivalent to an investor mortgage rate increase.

As stated in the CBA Updated Housing Outlook (May 2026): "Removing negative gearing is equivalent to roughly a 90 to 155 basis point increase in investor mortgage rates in immediate cash flow terms." This is comparable to the entire RBA tightening cycle of 2022-23.

Can indexation be more generous than the old 50% CGT discount?

For long-hold investors at current inflation rates, yes. Indexation inflates the cost base every year, so the longer you hold, the more of your nominal gain is treated as inflation rather than real gain, and therefore not taxable.

In a 20-year metro-new-build scenario modelled by Get RARE Properties, the new indexation method saves approximately $15,000 in CGT compared to the old 50% discount. The previous discount was never inflation-adjusted; indexation is.

When does the trust restructuring rollover window close?

The expanded rollover relief is available for three years, from 1 July 2027 to 30 June 2030. Discretionary trusts can use this window to restructure into another entity type (typically a company or fixed trust) without triggering CGT.

Engaging an accountant in 2026 rather than closer to the deadline is recommended, as advisor capacity will be constrained closer to the 30 June 2030 close.

Has the Federal Budget 2026 property reform been passed into law?

No. As at 15 May 2026, all three measures (negative gearing, CGT discount replacement, 30% trust tax) are announced but not yet law. They remain subject to consultation and parliamentary passage. Treasury fact sheets have been published, but draft legislation has not yet been released.

Investors should plan and document now but avoid making irreversible decisions (selling, restructuring, buying) until the law is finalised.

What investors said about the briefing

From attendees and long-term clients.

A handful of unsolicited notes received after Thursday's session, plus broader feedback from people who have worked with Rasti and the team over time.

Rasti provided a great deal of information on the impact of the budget on property investing that I found really useful. As the rules adapt, Rasti and his team were able to look at the alternatives available and provide guidance as to how best to invest efficiently.

BK

BK

Budget briefing attendee

Great session. Wanted to appreciate that we have the best team with you and Manpreet as our accountant. Don't see any issues going forward in our long-term relationship.

GS

Gaurav Sharma

Long-term Get RARE & AceBiz client

The sessions are practical, easy to follow, and grounded in real-world investing strategies rather than hype. Rasti does an excellent job of breaking down complex economic and political jargons into simple language that everyday people can actually understand and apply. Highly valuable for anyone looking to build confidence in property investing.

DS

Deepak Sahu

Masterclass attendee

Co-presented by

Two specialists. One conversation.

This briefing was delivered jointly. The strategy decision and the tax structure decision come from two different disciplines. We built the session so you would get both in the same room.

Rasti Vaibhav, CFA

Founder · Get RARE Properties

Award-winning buyer's agent. CFA Charterholder with an MBA from the University of Chicago Booth School of Business. Former institutional quantitative fund manager at Westpac and AMP Capital, where he managed portfolios exceeding $2 billion.

Has helped over 500 Australian families build portfolios worth more than $300M. Owns 21 investment properties across four states. Named one of Australia's Top 50 Small Business Leaders in 2025.

CFA CharterholderMBA · Chicago Booth$300M+ guided

Manpreet Singh, CA

Chartered Accountant · AceBiz

Property tax and structuring specialist with more than 20 years' experience. Partner at AceBiz Accounting, advising over 800 clients annually across tax, structuring, SMSF and business advisory.

Deep expertise in tax-efficient ownership structures including trusts and SMSFs. Has saved clients thousands in tax through proper structuring, with a focus on protecting and growing wealth long-term.